Our portfolio positioning in recent months is decidedly more cautious. Cash holdings are elevated so that we are ready to snap up bargains in risk assets as market volatility provides opportunities.

Interest rates have dropped this year as stalling economies and heightened uncertainties encouraged central banks to return to more accommodation. Bond yields declined as the more pessimistic outlook encouraged a flight to safety and equity markets rallied through higher multiples despite softer earnings.

Together these forces encourage us to be slightly underweight equities and property where only limited value is on offer. We are modestly underweight US and Australian equities which offer least value, neutral Europe where economic performance may surprise on the upside and overweight Japan which is being largely overlooked by international investors. Equities can continue to advance in the next several years, but we continue to increase quality diversification and value in our portfolios at every opportunity.

We are wary that more investors are taking on even greater risk to achieve a targeted return by chasing higher-yielding stocks or lower-rated credit at higher valuations. The poor performance of recent initial public offerings such as Uber and Lyft and the pulling of WeWork, Latitude Financial and PropertyGuru IPOs may be a sign that the market is becoming more concerned about paying high multiples for growth businesses.

The valuation discrepancy between “growth” companies delivering sustained earnings growth and “value” stocks that have more cyclical earnings profiles has become even more stark in recent months. There is a high prevalence of companies in information technology or healthcare sectors trading on earnings multiples of 30 times or more. By contract, several names in energy, financials and materials trade on multiples in the 12 to 15 times range.

Heightened concerns over the possibility of recession have encouraged a flood of money into so-called “defensive” areas like consumer staples and utilities. However, their lofty valuations mean they may not be defensive investments at all. In time they may perform relatively poorly.

Our preference for high quality results in a natural inclination toward “growth”. However, there are several “value” names in which we have taken positions because of the enticing prospective returns left on offer by a short-term focused and overly pessimistic market. Some of these are more exposed to cyclical forces than other companies we own, and their share prices are more volatile as a result. However, each is well placed in its industry for longer term success and offer compelling prospective returns for patient investors like us. Their share prices should perform well if the markets start to reduce expectations for a near term recession and if bond yields continue to rise.

As wages continue their upward momentum, prices in general will start to rise, bond yields will rise and central banks in the US and Australia will be forced to shift to a tightening stance. We are underweight the fixed interest asset class and our exposures have shorter duration (or interest rates sensitivity) than the benchmark. Given our focus on capital preservation, the bulk of portfolio holdings are in government securities. We hold only small exposure to corporate bonds, much of which is hedged by longer duration government bond positions.

Manufacturing weak. Consumption solid

Global economic growth has hit a significant downdraft which is likely to worsen during the remainder of the year. Trade and geopolitical conflicts have raised uncertainties while demand is being weighed by structural factors like low productivity growth, tightening labour markets and aging advanced-economy populations.

Weakness in manufacturing and business investment have started to weigh on services activity which until now has been solid. Declines in business and consumer confidence point to a period of constrained spending. Automotive activity has been particularly weak due to new emissions standards in Europe and China and tighter industry lending practices.

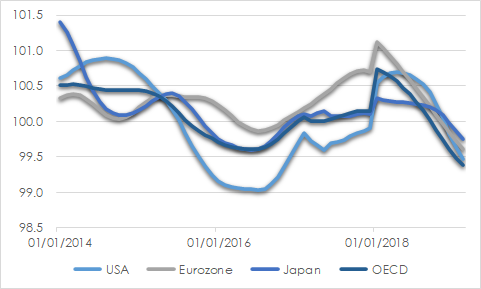

The Conference Board’s Leading Economic Indicators Index, which is intended to provide early signals of turning points in economic cycles, has continued its downward trend since mid-2018. The weakening environment makes corporate earnings growth harder to achieve and there is downside risk to earnings expectations particularly if trade conflicts worsen.

CHART 1: LEADING INDICATORS

Source: Conference Board

Despite prevailing challenges however, activity should stabilise through next year on further employment and wages gains which will encourage services activity. Recent monetary accommodation will support interest rate sensitive sectors. Investment should steady through 2020 so long as trade tensions do not worsen.

United States activity is being helped by solid consumption, improving housing and steady car sales. Europe has been hit hard by weak export demand and Brexit distractions, but domestic demand remains solid and there are early shifts toward increased fiscal support. Japan’s growth is likely to be even slower as new fiscal action helps offset the impact of the increased consumption tax.

China growth remains above that of much of the world, although it is slowing due to trade friction, efforts to contain debt expansion and the shift to consumption-led growth. Monetary and fiscal policies have been expanded to help lift consumption, property construction and infrastructure spend to offset weakened exports and private investment. GDP growth should improve modestly in the December 2019 quarter though we expect official China GDP growth to slip below 6% next year.

While we expect global growth to continue through next year, protectionist policies could make it a bumpy ride. There could be a sharper deterioration in conditions if corporates respond to the increased uncertainties by reducing spending on capital equipment and jobs. However, escalation of the conflict is unlikely ahead of 2020 US presidential elections. Both sides would benefit from an easing in tensions – Mr Trump to improve re-election prospects, China to improve growth prospects.

A complete rollback of the recent tariff increases probably requires agreement from China to undertake significant structural reforms. This appears unlikely at least in the short term. Highly contentious issues remain including in relation to intellectual property law and technology transfers. There are also several other sources of tension not directly related to trade that make the achievement of a substantial US/China deal appear a long way off, such as alleged currency manipulation, 5G network development, Hong Kong unrest and questions over human rights violations.

Return to monetary stimulus supportive now but increases longer term vulnerabilities

Central bank easing in recent months despite low unemployment, wages growth and reasonable economic expansion, should help extend the cycle through next year.

The US Federal Reserve made a significant about-face in policy this year. After several years progressively tightening financial conditions, the Fed has shifted to more accommodation. The federal funds rate has been cut by 25 basis points each in August, September and October, to the current range 1.50% to 1.75%. At least one or two of these cuts are likely to be proven unnecessary and leave less ammunition to fight the next downturn. Unemployment is 3.6%, GDP growth is solid, and inflation is close to the 2% target. Core PCE inflation is 1.8%.

The Fed’s moves have encouraged other central banks around the world to also ease policy and this has prompted further appreciation of the US dollar.

US Federal Reserve committee members have been ignoring incoming economic data, concerned more with possible downsides from trade negotiations, Brexit and financial markets volatility. The first two of these are beginning to subside but financial markets turbulence could well increase in the coming year.

The US Federal Reserve appears to be shifting back to a data-dependent approach. A further 25 basis point cut early next year is possible, but only if the US economy starts slowing more than expected. Greater challenges lie ahead for committee members through next year as inflation drifts above the 2% target, helped by wage increases, new tariff costs and base effects of comparisons to soft prior year numbers. Bond yields are likely to steadily increase which will be unsettling for equity markets.

Concerns about the downsides of very low interest rates are justified. Many savers are trying to fund their long-term spending plans, such as in their retirement years. Given aging populations and ultra-low interest rates, more people need to save even more money rather than consume. Negative or extremely low interest rates also encourage increased risk-taking by investors seeking targeted returns. Financial vulnerabilities are increased.

Andrew Doherty. AssureInvest

This article is provided as general information only and should not be construed as personal financial advice.

Contact Us

Let us demonstrate how we can deliver outstanding outcomes for you.

p +61 2 8094 8410

e [email protected]

About AssureInvest

AssureInvest is your trusted professional investment partner. We offer a holistic and successful investment approach and carefully tailored solutions for individual needs, as well as cost saving innovations, integrity at the highest level and attentive customer service.

Our advisor clients are empowered to boost their profits and deliver better investment outcomes, benefiting their clients and the broader community.

Our disciplined and long term focus provides a critical framework for assessing new value-adding opportunities, preserving capital, generating superior returns and implementing at low cost.

Copyright

© 2019 AssureInvest Pty Ltd (ABN 55 636 036 188 AFSL number 478978). No part of this publication may be reproduced or distributed in any form without prior consent in writing from AssureInvest.

Disclaimer, General Advice Warning and Disclosure

The data, information and research commentary in this document (“Information”) may be derived from information obtained from other parties which cannot be verified by AssureInvest and therefore is not guaranteed to be complete or accurate, and AssureInvest accepts no liability for errors or omissions.

The Information constitutes only general advice. In preparing this document, AssureInvest did not take into account your particular goals and objectives, anticipated resources, current situation or attitudes. Before making any investment decisions you should review the product disclosure document of the relevant product and consult a securities adviser. Past performance is no guarantee of future performance. This document is not intended for publication outside of Australia.

This document is current until replaced, updated or withdrawn and will be updated if the information in it materially changes. Please refer the AssureInvest Financial Services Guide (FSG) for more information.

This is available at: assureinvest.com.au/wp-content/uploads/2016/05/FSG_AssureInvest_Dec-2015.pdf.

AssureInvest personnel may own securities referred to in this document. They do not receive compensation related to the information or commentary in this document.

FREE Special Report: How to Jump ahead of competitors and add more value for clients

Learn how you can boost profits while enhancing customer outcomes.